By Anthony Summers, Wealthy Retirement, 2024-04-26

In a market that often feels like a casino, it's refreshing to find stocks that consistently deliver impressive results year after year.

One such company is Kimberly-Clark (NYSE: KMB), the consumer staples giant behind iconic brands like Kleenex, Huggies and Cottonelle. This dividend dynamo has been a reliable wealth compounder for generations, so I decided to put it through my Value Meter.

Valuation

The company currently trades at an enterprise value-to-net asset value (EV/NAV) ratio of 48.7. At first glance, that may seem astronomically high compared with the average EV/NAV of 6.8 among similar companies.

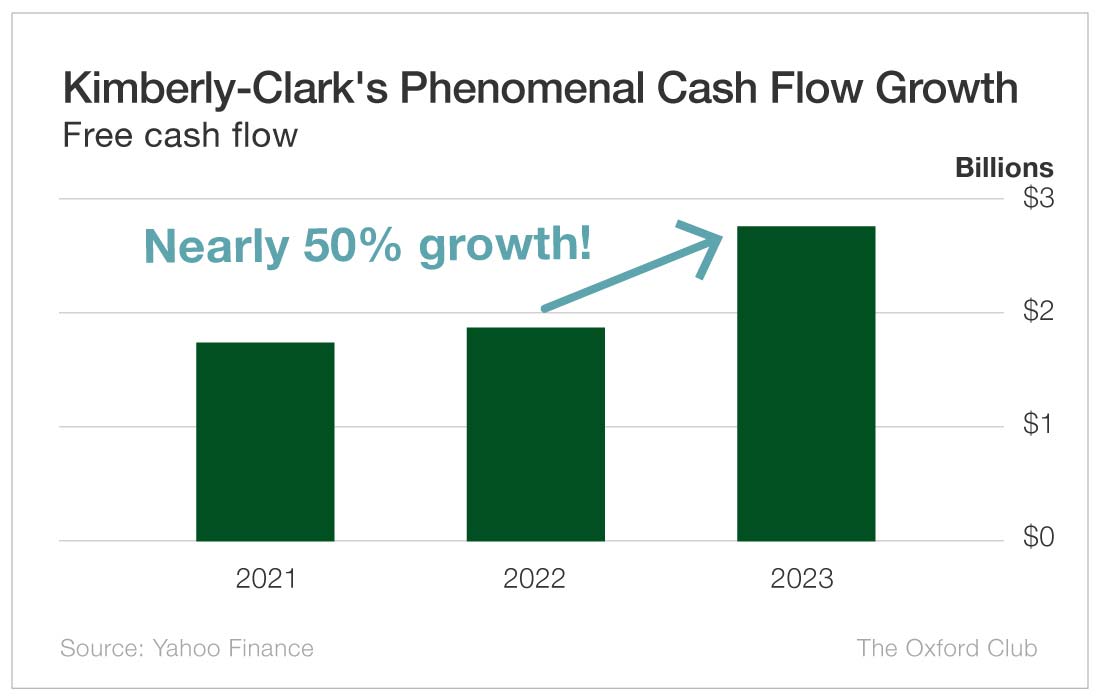

However, when we consider Kimberly-Clark's extraordinary cash generation capabilities, its valuation becomes more justifiable.

Cash Flow Growth

Last year alone, the company grew its free cash flow by almost 50% – from under $1.9 billion to nearly $2.8 billion.

Even more impressively, over the past four quarters, the company's free cash flow averaged an astonishing 745.9% of its net asset value. To put this in perspective, the average for companies with a similar cash flow history is a mere 8.6%.

In other words, Kimberly-Clark has generated cash relative to its net assets at a rate nearly 100 times that of its peers.

Put simply, it's in a league of its own.

Dividend Track Record

This robust cash flow is the driving force behind Kimberly-Clark's remarkable dividend track record. The company is a proud member of the “Dividend Aristocrats” club, an elite group of S&P 500 companies that have raised their payouts for at least 25 consecutive years.

But Kimberly-Clark has far surpassed that threshold. It has an impressive streak of 53 years of uninterrupted dividend hikes. The stock currently boasts a forward dividend yield of 3.5% and a manageable payout ratio of 65.8% of forward earnings, so it has ample room to continue its dividend growth.

Latest Quarterly Results

And the company's latest quarterly results only strengthen the bullish thesis.

In Q1 2024, Kimberly-Clark reported net sales of $5.1 billion and organic sales growth of 6%, which was driven by a combination of price increases and volume gains. Additionally, gross margins expanded year over year to 37.1% thanks to strong operating leverage, productivity improvements and lower input costs.

Diluted earnings per share (EPS) also jumped 14% year over year to $1.91, crushing analyst estimates.

Outlook and Initiatives

Looking ahead, management has raised its full-year outlook, now projecting mid-single-digit growth in organic sales and low double-digit growth in EPS for 2024. And its “Optimize Margin Structure” initiative, which aims to digitalize the supply chain and boost efficiency, is expected to generate more than $3 billion in gross productivity and $500 million in working capital savings.

If successful, these efforts should help mitigate any short-term headwinds.

The company's latest results and its optimistic forecast showcase its ability to weather challenging market conditions while being proactive and staying ahead of the curve.

Shareholder Value

It's also worth noting that the company is increasing shareholder value through brand acquisitions and share buybacks.

While Kimberly-Clark may not be a high-flying growth stock, it offers investors a rare combination of stability, income and long-term growth potential in an increasingly uncertain market. For patient investors seeking a reliable addition to their portfolios, it is a stock worth considering.

Valuation Conclusion

The Value Meter rates Kimberly-Clark as being “Slightly Undervalued.”